Understanding Debt

Debt is a ubiquitous element in both personal and business financial landscapes. It typically entails borrowing funds with the commitment to repay the principal amount along with interest over a certain period. Understanding the complexities of debt is crucial, as various types of debt exist, each with distinct implications. Broadly, debt can be categorized into “good debt” and “bad debt,” terms that help individuals and businesses in making educated financial decisions.

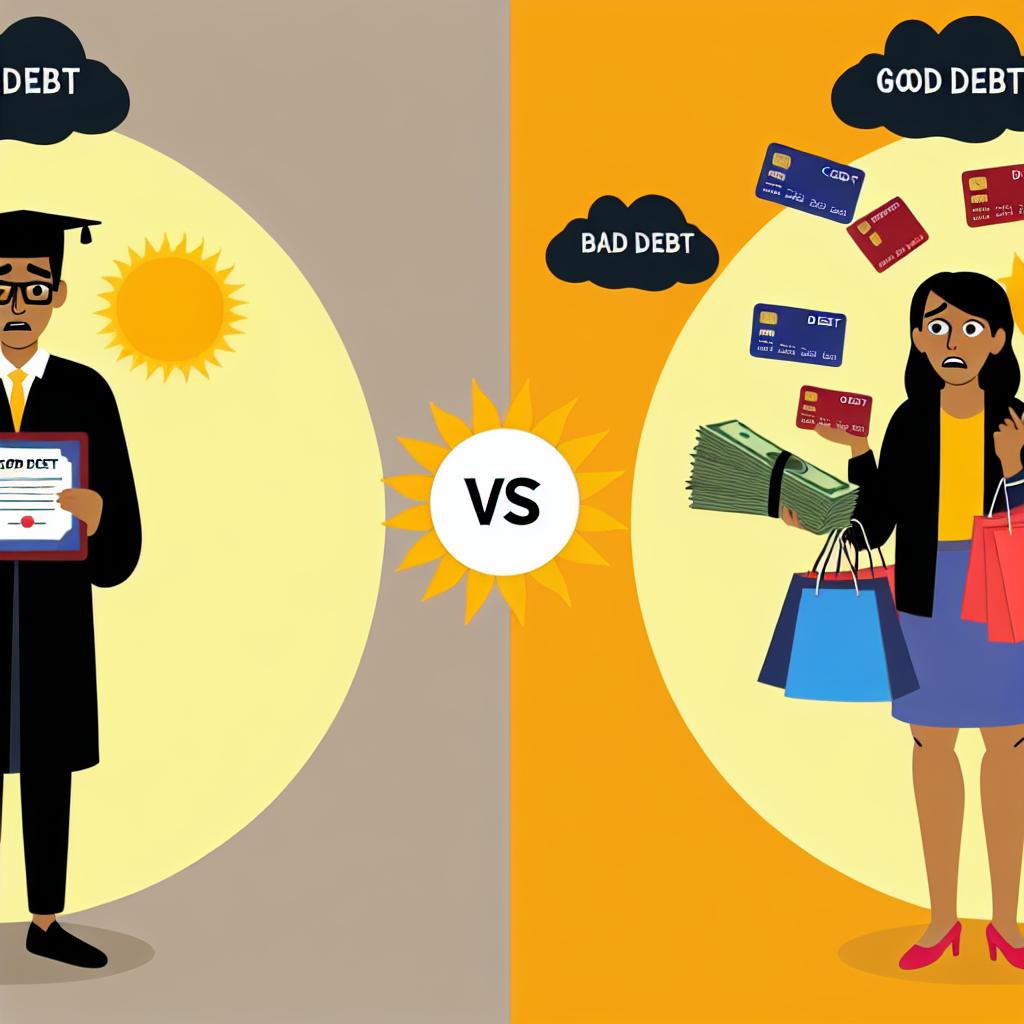

What is Good Debt?

Good debt generally refers to borrowing that is perceived as an investment in the future, often resulting in added value or income generation over time. Recognizing its potential benefits can lead to more informed borrowing choices.

Mortgage Loans: A common example of good debt is a mortgage loan used for purchasing real estate. The underlying asset in this transaction, the property, is expected to appreciate over time, making this type of debt beneficial. Homeownership comes with various financial advantages, such as potential tax deductions and avoiding rental costs. Further, real estate can serve as a stable investment, offering appreciation and equity build-up.

Student Loans: Another form of good debt is student loans, which finance education. Investing in education can open doors to better career opportunities, ultimately leading to improved income potential. The skills and qualifications gained through higher education typically enhance employability, making this debt a pathway to long-term financial security and professional growth.

Business Loans: Loans used for business expansion or operational improvements are also considered good debt. By investing in a business, individuals or companies can stimulate growth, profitability, and market competitiveness. When managed effectively, business loans can support strategic initiatives like expansion, acquiring new technology, or funding marketing campaigns, all contributing to sustained success and financial viability.

Advantages of Good Debt

Good debt has multiple advantages when approached strategically. It generally involves a clear repayment strategy and a substantial return on investment. Responsible management of good debt can improve credit scores, ensuring access to better lending terms in the future. It also facilitates the leveraging of financial opportunities that can enhance one’s financial standing and potential for wealth accumulation.

Understanding Bad Debt

In contrast, bad debt denotes borrowing for purchases or expenses that neither appreciate in value nor generate income. Such debt often results in financial strain and challenges due to its consumption-based nature.

Credit Card Debt: Credit cards, though convenient, can lead individuals into high-interest debt if not managed carefully. The allure of credit cards is their ease of use, but without a strategic plan or budget for repayment, they often result in financial difficulties. High-interest rates and lack of tangible assets or returns categorize this as bad debt.

Payday Loans: These short-term, high-interest loans are notorious for trapping borrowers in cycles of debt. The elevated fees and interest rates associated with payday loans make them particularly risky, especially if not paid back promptly. They can become a significant financial burden if relied upon regularly.

Car Loans: While essential for transportation, car loans typically fall under bad debt due to vehicle depreciation. Unlike real estate, automotive assets diminish rapidly in value, and the associated debt rarely contributes to income generation or value appreciation. While necessary for many, it’s crucial to recognize the financial implications of car loans.

Disadvantages of Bad Debt

Bad debt poses various risks and drawbacks. The high-interest rates and potential for a borrowing cycle without significant financial return can create persistent financial challenges. Importantly, bad debt does not contribute to income generation or asset accumulation. Poor management of such debts can lead to adverse effects on credit scores, limiting future financial opportunities.

Balancing Good and Bad Debt

Achieving financial health involves striking an optimal balance between good and bad debt. Careful consideration before taking on debt is vital, ensuring a clear repayment strategy and understanding of long-term impacts. Evaluating aspects such as interest rates, loan terms, and potential returns allows for informed decision-making. Through deliberate debt management, individuals can avoid the pitfalls associated with excessive borrowing, promoting sustained financial well-being.

Conclusion

In conclusion, while certain debts can effectively support future financial growth and development, others can lead to financial burdens and hardship. Differentiating between good and bad debt and managing them prudently is a cornerstone of achieving financial stability and health. By making informed choices and implementing disciplined management practices, individuals and businesses can leverage debt to their advantage, steering towards a secure and prosperous financial future.

This article was last updated on: March 10, 2025